Resources

Ecom-Energy’s April 2021 Natural Gas Market Update

As the U.S enters the natural gas injection season, short-term (12-month) contracts continue to carry a premium thanks to lackluster production and less than ideal storage.

As the U.S enters the natural gas injection season, short-term (12-month) contracts continue to carry a premium thanks to lackluster production and less than ideal storage.

With production falling and storage near the five-year low, short-term gas deals are likely to carry a premium. Work with an objective expert like Ecom-Energy to get the most competitive prices available.

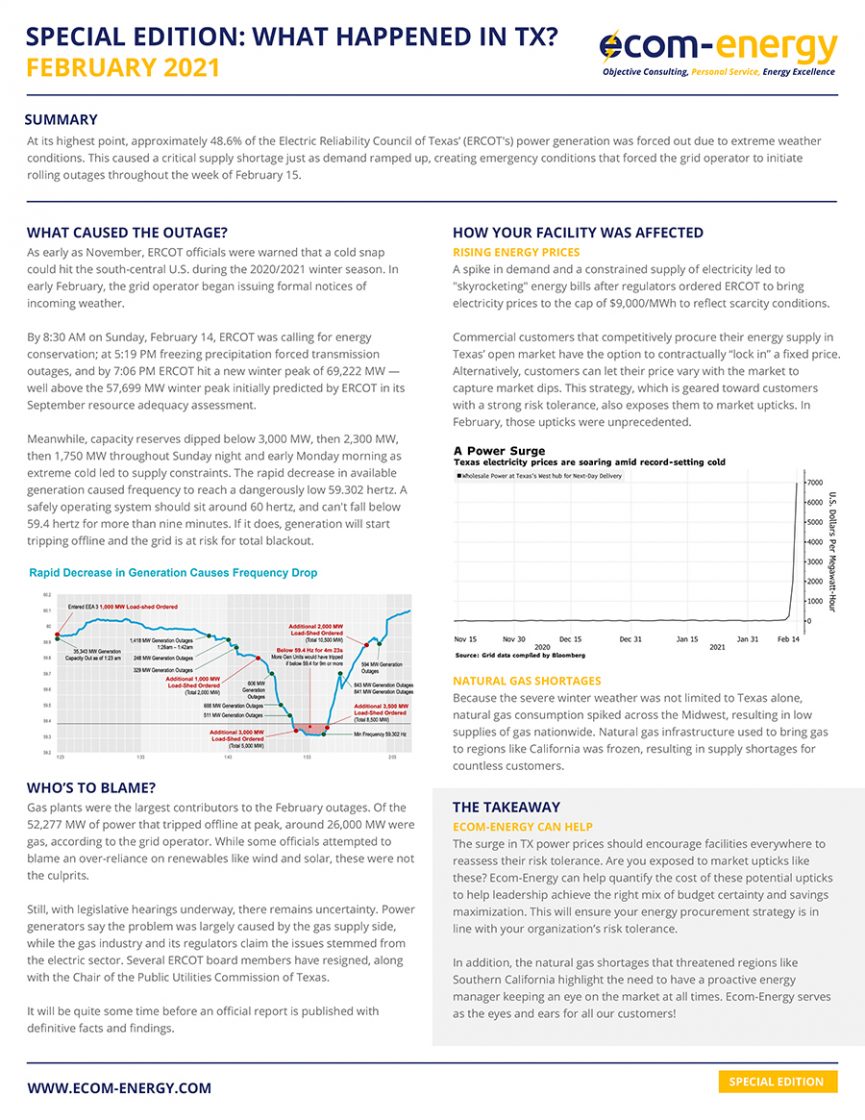

At its highest point, approximately 48.6% of the Electric Reliability Council of Texas’ (ERCOT’s) power generation was forced out due to extreme weather conditions. This caused a critical supply shortage just as demand ramped up, creating emergency conditions that forced the grid operator to initiate rolling outages throughout the week of February 15.

Increased domestic industrial energy use, coupled with strong and ongoing demand for U.S. exports, could drive natural gas prices higher in 2021.

A combination of winter weather and working from home (increased residential demand) have lifted prices to double their summer lows.

Coming months will be driven by lower domestic production, winter demand, and increasing LNG exports – causing price increases.

With many unknowns, facilities should reassess their risk tolerance to ensure it aligns with their procurement strategy.

An abundance of natural gas in storage with moderate production means weather will be the primary pricing driver as summer wears on. July is expected to be warmer than average for most of the U.S.

With well-stocked natural gas storage inventories, weather will be a primary pricing driver heading into the summer months.

COVID-19 and the collapse of oil prices have reduced both supply and demand for natural gas. Price rallies and volatility have materialized, though not to the degree some would expect.

Mr. Burks is Ecom-Energy's Manager, Renewables & Generation. Aric comes to Ecom-Energy with a diverse background in multi-state alternative vehicle funding & incentive tracking, alternative fuels grant writing, supporting non-profit sustainability climate action, as well as city planning and project evaluation. Aric also has worked to streamline Environmental Health & Safety Compliance Practices across multiple hospitals.

Aric completed both his Master's of Science in Sustainability Solutions and his Bachelor of Science in Sustainable Energy, Materials, and Technology at Arizona State University. Aric is also an alumnus of the INROADS Organization.

Mr. Lopez II is Ecom-Energy’s Managing Principal. Carlos carries over a decade of energy management experience and is a member of ASHE & CSHE (California Society of Healthcare Engineers), IFMA (International Facility Management Association) and AEE (Association of Energy Engineers) where he earned his CEP (Certified Energy Procurement Professional), REP (Renewable Energy Professional), BEP (Business Energy Professional), and CSDP (Certified Sustainability Development Professional) designations.

Mr. Lopez II joins Ecom-Energy after completing a Bachelor’s in Business Administration and a Minor in Biblical Studies from Barclay College in Kansas, where he also played soccer. Prior to finishing his education, Carlos II was a Case Administrator at Judicate West, one of the leading Alternative Dispute Resolution firms in California.

Yasmeen Qursha

Ms. Qursha is Ecom-Energy’s Manager of Energy & Sustainability. Yasmeen brings experience as the previous Unit Director for the Center for the Environment at UC Davis, focused on transforming the campus to a zero-waste campus. Relatedly, Yasmeen also served as Commissioner for the Environmental Policy and Planning Commission and worked on green policies to contribute to system sustainability. Yasmeen is a member of ASHE & CSHE, and AEEand alsobrings several years of experience in the non-profit sector managing projects serving marginalized communities.

Yasmeen completed her Bachelor of Science in Environmental Policy Analysis and Planning with a focus in Energy and Transportation Planning from the University of California, Davis.

Intern

Jin is joining Ecom-Energy, Inc. as an intern assisting in Energy & Sustainability services. Jin is currently completing her Master of Science in Environmental Studies from California State University, Fullerton in Spring 2024. She recently received her Bachelor of Arts in Environmental Science from the University of California, Irvine.

Jin comes with previous experience in supply chain project management in the retail sector, with a focus on product quality control. Jin also worked as a Production Coordinator at Orange Circle Studio and served as a Group Leader at Compass Ministry.

Mr. Lopez is Ecom-Energy’s Principal. Prior to joining the Ecom-Energy Team, Carlos Sr. was responsible for developing and implementing integrated energy solutions for commercial, institutional and industrial clients at NORESCO, an Equitable Resources Company. His responsibilities included orchestrating energy efficiency programs, including demand-side management, performance contracting, information services and financial options.

Previously, Mr. Lopez was Manager – San Diego Region for AES New Energy. In this position, Mr. Lopez was responsible for working with clients to develop and implement energy initiatives associated with the deregulation of the electricity marketplace – including competitive direct access, distributed generation and information technology.

Mr. Lopez has worked extensively with healthcare providers and is a member of the California Society of Healthcare Engineering (CSHE), where he has given numerous presentations and seminars on the deregulation of the electricity market in California.

Matthew Dietz

Mr. Dietz is the EnerVisor Software Manager for Ecom-Energy. Matthew comes to Ecom-Energy with over 11 years of experience in software and code development and implementation. He is a Microsoft Certified Specialist and worked as a certified teacher for Excel and data management. Prior to joining Ecom-Energy, Mr. Dietz served as the Principal System Administrator focusing on Network Engineering, and a Program Analyst within the Tustin Unified School District.

Matt received a PhD in Astrophysics from Chapman University after attending Hope International University and earning a Bachelor of Science in Biblical Studies.

Wesley Haugen

Mr. Haugen is Ecom-Energy’s Senior Project Manager. Wesley comes to Ecom-Energy with over 15 years of experience in Finance & Commercial Real Estate. During his tenure, Wesley held assorted positions responsible for asset management protection, appraisal management, financial market review, policy creation, credit worthiness assistance and was a California State Licensed Real Estate Agent, Real Estate Appraiser and member of the Appraisal Institute.

Mr. Haugen attended California State University, Fullerton earning a Bachelor of Arts in Business Administration with an emphasis on Finance.

Dilip R. Limaye

Mr. Limaye is Ecom-Energy’s founder. Mr. Limaye was formerly President of SRC International (SRCI), a worldwide research and consulting firm specializing in efficient management and utilization of electricity, gas and other natural resources. Mr. Limaye directed a number of pioneering projects related to energy efficiency, demand-side management (DSM), on-site generation and cogeneration, and energy service companies (ESCOs).

Mr. Limaye was also the Founder and President of the International Energy Services Company (INTESCO), the first multinational ESCO. He guided INTESCO’s activities in Asia, Eastern Europe and Australia. He has provided consulting services and technical assistance related to business strategies, financial plans, start-up and operation to 12 utility affiliated ESCOs in the U.S., Canada, and Sweden.

Ms. Dietz is Ecom-Energy’s Energy Analyst. Tiffini comes to Ecom-Energy with several years’ experience in the health care industry along with an expansive IT background specializing in programing and data management.

Ms. Dietz attended Ohio Christian University graduating highest honors with a Bachelor of Arts in Christian Ministry and Leadership. She also attended Southern New Hampshire University majoring in Creative Writing.